WAGES have risen at their fastest rate on record, the Office for National Statistics (ONS) has said.

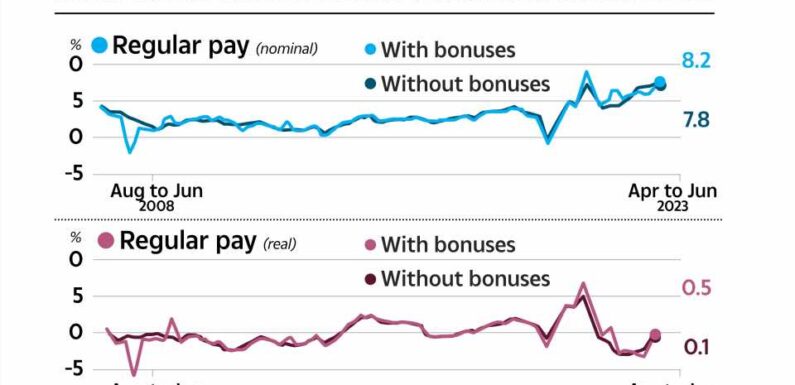

Official figures today reveal regular pay excluding bonuses stood at 7.8% in April to June this year.

It's the highest regular annual growth rate the ONS has seen since records began in 2001.

Average total pay, which included bonuses, was 8.2%, which was affected by a one-off bonus paid to NHS staff in June.

It means wages are rising at a faster rate. Last month regular pay went up by 7.3%, and 6.9% including bonuses.

Darren Morgan, director of economic statistics at the ONS, said: "Earnings continue to grow in cash terms, with basic pay growing at its fastest since current records began.

Read more in money

Brits face high interest rates into 2025 as BoE grapples to contain inflation

I was on huge Netflix reality show but can’t afford a house or a car

"Coupled with lower inflation, this means the position on people's real pay is recovering and now looks a bit better than a few months back."

However, taking into account inflation means that wages only rose by 0.5% for total pay and 0.1% for regular pay in real terms.

Wages have been rising at less than the rate of inflation in previous months.

When prices rise by more than pay, it squeezes people's incomes, leaving them with less money to spend.

Most read in Money

Martin Lewis' MSE issues urgent warning to everyone with a savings account

I tested supermarket beans – winner was 95p cheaper than Heinz & tastier

Wilko bidders revealed in race to save chain with under 48 hours to go

Wilko shelves empty – shoppers are all saying the same thing about it closing

The latest wage figures show some of this pressures on household budgets could ease.

But rising wages could force the Bank of England to hike rates again as it tries to bring inflation back down to its 2% target.

The rate of UK unemployment increased in the three months to June even as pay grew at the fastest rate since records began, according to the ONS.

Unemployment rate hit 4.2% during the quarter, up 0.3 percentage points from the previous three-month period.

It is the highest since the three months to October 2021, the ONS said, and brings the measure above pre-pandemic levels.

Chancellor of the Exchequer Jeremy Hunt said: “Thanks to the action we’ve taken in the jobs market, it’s great to see a record number of employees.

“Our ambitious reforms will make work pay and help even more people into work – including by expanding free childcare next year – helping to deliver on our priority to grow the economy.”

What does it mean for my money?

The main concern when workers see a "real-terms" fall in their salary is that it's not keeping up with the cost of living.

It means people's pay packets have fallen in real-terms, when factoring in other living costs such as food and energy.

Wage growth has been lower than inflation, as prices of everything from groceries to energy bills increase at a faster rate.

But inflation has started to fall, easing pressure on households.

The UK's rate of inflation dropped more than expected to 7.9% in June this year.

The Consumer Price Index level of inflation decreased from 8.7% in May.

City economists had predicted that last month's inflation would fall but to 8.2%, so it is lower than expected.

Inflation is a measure of how the price of goods and services has changed over the past year.

Grocery inflation slowed to 16.5 per cent, the lowest level since the start of the year but still one of the highest levels in 15 years.

Jack Kennedy, senior economist at Indeed, said: "There are signs the cost of living could finally start to ease after record annual pay growth drove pay above inflation for the first time in over one-and-a-half years.

"While the wage growth figures will grab attention, the ONS data also showed the labour market continuing to rebalance.

"The unemployment rate jumped by a larger than expected 0.3 percentage points to 4.2%, driven by an increase in long-term unemployment and more people moving out of inactivity."

It means you will be feeling the pinch as your income doesn't go as far and may end up struggling to pay your bills.

Rising wages have been blamed for actually keeping inflation high by Bank of England bosses.

Earlier this month, the BoE hiked rates yet again to a new 15-year high.

The last time it stood at 5.25% was in March 2008.

The Bank’s Monetary Policy Committee (MPC) has lifted the base rate by 0.25 percentage points to 5.25%

High-street banks use the BoE base rate to work out the interest rates it offers to customers.

A further hike means the cost of borrowing, including loans, credit cards and mortgage repayments could become more expensive.

Read More on The Sun

Tributes to girl, 10, found dead at home as international hunt continues

X Factor star looks unrecognisable as Fearne Cotton marks his birthday

Consecutive hikes from historic lows have piled pressure on homeowners, with more to come if they rise again.

The government has brought in more support for those struggling with higher monthly payments, including extending the term of their mortgage and moving to interest-only repayments.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

You can also join our new Sun Money Facebook group to share stories and tips and engage with the consumer team and other group members.

Source: Read Full Article