Treasury minister warns Brits need to suck up mortgage pain to tackle inflation – as he tees up squeeze on ‘struggling’ public services with government’s £2.6tn debt pile ’16 times the NHS budget’ and interest costs now £100bn a year

The government’s £2.6trillion debt mountain is like a ‘national mortgage’ and the books are being hammered by soaring interest rates, a Treasury minister warned today.

Chief Secretary John Glen made clear that Brits will need to suck up the pain, suggesting the Bank of England must prioritise inflation because it is a ‘tax on everything we buy’.

But writing for MailOnline, Mr Glen gave a stark assessment of the impact on the public finances, with the debt pile equivalent to 100.1 per cent of GDP – or 16 times the annual NHS budget.

Highlighting that the government is now facing interest payments of £100billion this year as rates soar, Mr Glen put the public sector on notice that it must get ‘more efficient’.

‘We need to make sure we are getting bang for taxpayers’ buck. While the private sector has rebounded admirably from a once-in-a-lifetime pandemic, the public sector is still struggling. That needs to change,’ he wrote.

Writing for MailOnline, Chief Secretary to the Treasury John Glen made clear that Brits will need to suck up interest rate pain, saying that the Bank of England must prioritise inflation because it is a ‘tax on everything we buy’

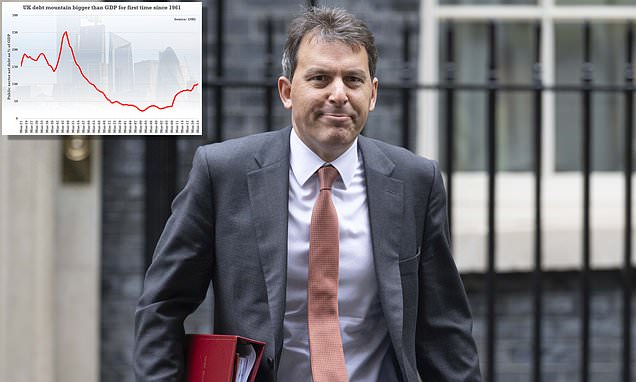

Net debt hit 100.1 per cent of GDP in May as government borrowing more than doubled compared to last year

The intervention will raise questions about whether the government still feels it can go ahead with mooted pre-election tax rises – despite a desperate clamour from Tory MPs.

Net debt hit 100.1 per cent of GDP in May as government borrowing more than doubled compared to last year.

It is the first time the debt-to-GDP ration has risen above 100 per cent since March 1961.

The threshold was initially thought to have been breached during the pandemic, but the ratio was later revised lower due to stronger GDP figures.

Borrowing reached £20billion for the month, pushed higher by the cost of energy support schemes, the benefits bill and interest payments.

May’s borrowing figure was £10.7billion higher than a year ago and the second-highest May borrowing since monthly records began in 1993.

Economists had predicted borrowing of £19.5billion for May.

John Glen: Struggling public services must get more efficient amid financial squeeze

Tomorrow the Bank of England face another difficult decision: whether to put up interest rates for the 13th consecutive time.

Doing so means higher costs for mortgage owners. Not doing so risks prolonging high inflation – a tax on everything we buy.

Inflation has led us to this point, showing exactly why we need to stick with our plan to halve it this year and get back to the two per cent target.

Higher interest rates also mean larger repayments on our national debt – which stands at a whopping £2.5trillion, a national mortgage worth sixteen times the annual NHS budget.

It was right to protect people against two global economic shocks in the form of the pandemic and Putin’s war, through furlough and one of the largest cost-of-living support packages in Europe.

But we’re now expecting to spend almost £100 billion on debt interest alone this year.

My job is to count every penny before government spends it and I find it incredibly frustrating to know that hard-earned taxpayer money will go to creditors rather than our NHS, schools and other services that need it.

That’s why alongside halving inflation we are doubling down on our pledge to reduce debt from its record high level.

The first part of our plan was to take difficult but responsible decisions to get spending in check, prioritising the things that really matter to people.

The decisions we’ve taken mean official forecasts now show that the deficit will be reduced in every year of the next five years while the latest projections for headline debt levels in 2027-28 are £50billion lower than expected back in November.

That’s a good start, but we need to stick to our plan to cut debt further.

We need to make sure we are getting bang for taxpayers’ buck. While the private sector has rebounded admirably from a once-in-a-lifetime pandemic, the public sector is still struggling. That needs to change.

Over the coming months I will work with colleagues across government to find ways that the public sector can work more productively.

Better productivity is the path to delivering better outcomes without necessarily spending more.

Finally, we need to grow the economy so we don’t have to rely on borrowing to pay for services. That’s why getting more people into work and unleashing business investment was a key focus of the Chancellor’s Spring Budget.

None of this takes away from the pain people are feeling today from both rising prices and higher mortgage costs.

But a stable economy, with lower inflation and debt, is the best way to deliver lower mortgage rates and ultimately improve living standards for everyone.

Source: Read Full Article